Scope 3 Emissions: The Next Frontier in Climate Engagements

November 11th, 2021 | John McHughan

In March 2024, the U.S. Securities and Exchange Commission (SEC) enacted the legislation that would require U.S.-listed companies to publicly report their climate-related risks and impacts. The long-awaited SEC Climate Disclosure Rules were released following months of intense public debate (including fierce opposition) and a record 24,000 comments submitted by companies, investors, auditors, legislators and other groups.

Now, and for the first ever time in the U.S., corporate climate disclosures would become mandatory in SEC filings and would be subject to the same level of scrutiny and audit requirements as for financial statements – ultimately putting climate disclosures on par with financial disclosures. In doing so, this groundbreaking ruling was intended to help make these climate disclosures “more reliable” and “provide investors with consistent, comparable, decision-useful information, and issuers with clear reporting requirements,” according to Gary Gensler, the SEC Chair.

However, the SEC made key omissions, including most notably, dropping requirements for the disclosure of value-chain emissions, otherwise known as Scope 3.*

*Scope 3 emissions are the result of activities from assets not owned or controlled by the reporting organization, but that the organization indirectly affects in its value chain.

Scope 3 emissions represent one of the Grand Challenges of Net Zero, and what the London Stock Exchange Group calls “one of the most vexing problems in climate finance.” These emissions are broad, spanning multiple sources upstream and downstream of company operations, and often across multiple tiers of suppliers and customers. They are also complex, as Scope 3 emissions are both costly and challenging to estimate, let alone measure directly. And often, they represent the overwhelming majority of a company’s overall emissions footprint. Increasingly, Scope 3 also represents a major obstacle for investors who are looking to cut financed emissions across their portfolios and meet net-zero commitments.

By excluding Scope 3, the SEC ruling has prompted companies and investors to wonder if this would be the end of Scope 3 disclosures for U.S. issuers and for corporate carbon accountability.

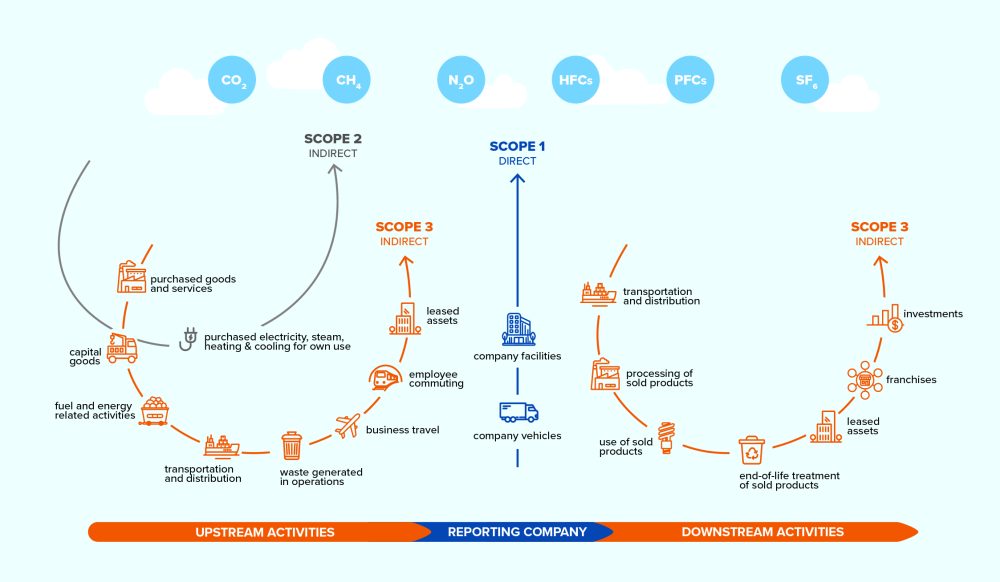

Here is a quick primer on Scope 3. Within carbon accounting, greenhouse gas (GHG) emissions are divided into three discrete ‘scopes’ based on where the emissions are created across a company’s operations and its wider value chain—as shown in Figure 1.

While companies have more control and influence over their Scope 1 and 2 emissions, Scope 3 emissions are generally more significant and result from companies’ supply chains (‘upstream Scope 3’) and use of companies’ products by consumers (‘downstream Scope 3’). Scope 3 is more complex for companies to track or estimate, but if gone unmanaged, may present financial risks, ranging from declining product competitiveness as consumer awareness for global warming increases, to higher cost of capital as insurers and investors aim to manage their own exposure.

Given the complexity and wide reach of these emissions, it comes as no surprise that globally, fewer companies report on Scope 1, 2 and 3 emissions, as compared to on Scope 1 and 2 alone – and U.S.-based companies in particular tend to lag on Scope 3 reporting.

However, the number of companies, both globally and in the U.S., that are reporting on their Scope 3 emissions has been consistently increasing year-over-year. According to the MSCI Net Zero Tracker, as at January 2024, approximately 42% of listed companies globally disclosed at least some of their Scope 3 emissions – a 17% increase compared to two years ago.

This disclosure trend is echoed by CDP. Of the 1,077 U.S.-based companies that reported on the CDP Climate Change questionnaire in 2023, only 13% did not report any Scope 3 emissions.

We see this trend reflected within our Mackenzie climate action engagements across U.S.-based issuers. Of the 100 companies with whom we engage via Mackenzie’s thematic climate engagement program, 41 are U.S. based, and of these companies:

– 44% have committed to SBTi (Science Based Target initiative) or set a SBTi validated target

– 41% have set GHG targets that include Scope 3 emissions

– 73% report in line with TCFD (Taskforce for Climate-Related Financial Disclosures)

– 76% report to CDP

From our climate engagement discussions, we are seeing a modest but consistent year-over-year increase in Scope 3 emission disclosure. Listed below are some notable examples of U.S. companies leading the way on disclosing and abating Scope 3 emissions.

Ahead of the pack: U.S. companies leading on Scope 3 disclosure, based on Mackenzie’s climate engagements

Marathon Petroleum Corp. (MPC) is a leading integrated, downstream energy company, based in Findlay, Ohio. Marathon reports on Scope 3 Category 11: Use of Sold Products,* which is the largest source of the company’s overall Scope 3 footprint. In addition to this, Marathon has also set a 2030 target to reduce absolute Scope 3 Category 11 emissions by 15% below 2019 levels on refined product. This target is informed by methodologies devised by the SBTi and Ipieca,** and aims to demonstrate the competitiveness of Marathon’s business within the global market.

Linde PLC (LIN) is one of the world’s largest industrial gases (such as ammonia and hydrogen) and engineering companies that is helping enable the clean energy transition. With operations spanning more than 80 countries, including the U.K. and the U.S., Linde is subject to various climate disclosure rules globally. Therefore, it’s not surprising that Linde currently reports on 14 categories of Scope 3 emissions representing all relevant categories for Linde. –About 40% of this inventory has been verified by a third party to the limited assurance level. Linde has set a SBTi-validated target to reduce its Scope 1 and 2 emissions and is working on emissions estimation and methodology development in anticipation of setting additional Scope 3 emissions reduction targets by 2026.

WEC Energy Group Inc. (WEC) is one of the largest electric generation and distribution and natural gas delivery group of companies in the U.S., based in the Midwest. WEC recently undertook an extensive review of all 15 categories of Scope 3 emissions across their organization to build the company’s first Scope 3 inventory. The disclosure was a cross-functional effort, relying on subject matter experts across WEC’s supply chain, finance, gas distribution, fuels, energy efficiency and environmental teams, and overseen by a dedicated Scope 3 Executive Steering Committee. WEC currently discloses multiple categories of Scope 3 through its ESG reporting.

Based on public disclosure and our own experience, company efforts to disclose and abate Scope 3 emissions continue even as the SEC removes its focus on Scope 3.

These emissions disclosure trends are being driven by several factors, but most notably by the shifting regulatory landscape around Scope 3 and the rise of climate disclosure rules globally.

During the two years that the SEC spent deliberating on the final rules, a suite of climate disclosure rules and standards emerged, all of which included provisions for the disclosure of emissions across a company’s Scope 1, 2 and 3. In 2023, the European Union’s (EU) Corporate Sustainability Reporting Directive entered into force, the International Sustainability Standards Board released its IFRS S2 standard, and the state of California passed the S.B. 253, the Climate Corporate Data Accountability Act.

We operate in a globalized economy – companies have global value chains, global consumers and global investors. Rather than seeing a form of ‘accounting arbitrage,’ and a race to the lowest level of disclosure when it comes to emissions reporting, what we predict is increased disclosures for companies that operate globally. Texas-based firms doing business in California or in the EU, for example, may now be required to disclose their Scope 3 emissions, regardless of the SEC final ruling.

We see this divergence in Scope 3 disclosure rules between the U.S. and other parts of the world as analogous to the longer-standing divergence between the US Generally Accepted Accounting Principles (US GAAP) and International Financial Reporting Standards (IFRS), where the U.S. decided to maintain their own accounting standards.

In the early 2000s, the International Accounting Standards Board released a new accounting standard, the IFRS, which was intended to establish global common accounting standards. However, the U.S. continued following US GAAP, leaving many U.S. issuers to report in adherence with both GAAP and IFRS.

We believe a notable paradigm shift has emerged regarding Scope 3 emissions reporting. Even if the SEC has dropped requirements for mandatory Scope 3 disclosure, U.S. issuers choosing to access global investors and supply chains will be required to adopt international climate disclosures. Ultimately, this leads us to believe that the direction of travel on Scope 3 disclosure is likely to be more, not less.

Contributor Disclaimer

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document includes statements that may be considered forward-looking information. Forward-looking statements are not guarantees of future performance or events, and involve risks and uncertainties. Do not place undue reliance on forward-looking information. In addition, any statement about companies is not an endorsement or recommendation to buy or sell any security. The content of this policy (including facts, views, opinions, recommendations, descriptions of or references to products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.