Is Nuclear Energy Suitable for an RI Portfolio?

May 12th, 2019 | Dominique Barker

According to the International Energy Agency, carbon-based electricity generation contributed over 30% of total global greenhouse gas emissions in 2018, by far the largest source of global GHG emission.

To minimize the impact of climate change and meet the Paris Agreement’s goal to limit the increase in global warming to 2°C, Morgan Stanley Research estimates that the world needs to spend US$50 trillion over the next 30 years in clean energy and technology. The International Renewable Energy Agency forecasts that US$750 billion a year is needed in renewables alone over the next decade.

The question on the minds of many investors is not whether to join in this growth, but how to channel capital into wind, solar, hydro-electric, bioenergy, energy efficiency and geothermal projects to help slow and mitigate climate change. Green bonds represent an exciting opportunity for socially and environmentally conscious investors, who want to make sure their dollars are going towards protecting and restoring the environment.

Investors can reduce the carbon intensity of their portfolios in many ways, through funds that exclude fossil fuels, integrate ESG factors, or focus on positive impact. Despite the positive aspects of these approaches, many funds do not provide a “pure play” into renewables, and often still include carbon intensive industries. Many clean energy focused funds invest in diversified utility companies which, in addition to their clean energy projects, also include significant amounts of fossil fuel generation and distribution. For investors that are seeking a “pure play”, there are two primary options to focus on: ‘pure’ renewable energy companies, such as publicly traded companies like Boralex, Brookfield Renewables, Innergex, and RE Royalties, and green bonds.

While investing in equity does present certain risk given the fluctuations of equity markets and performance of individual companies, green bonds present an alternative way to invest in the renewable sector by offering a more predictable fixed income style return. In contrast to buying shares and owning a piece of a renewable energy company, green bonds are a loan from the investor to a company to be used exclusively for investing in green projects.

The investor receives interest income on their investment (typically higher than a savings account or GIC) over a defined period of time, otherwise known as the term of the bond. At the end of the term, the investor receives the full value of principal back. In general, bonds are lower risk than stocks because the repayment takes legal priority (also known as seniority) above shareholder equity. That said, most green bonds are not secured against the projects themselves, particularly in the case of renewables. For more investor security, some green bonds are “senior secured” against the underlying assets, but these are rare (about 4% globally).[1] While green bonds offer more predictability and security, the one downside to green bonds is that they are usually illiquid, which means the investor usually must wait until the end of the term for the full principal to be returned.

The market for green bonds is expanding dramatically as investor sentiment towards environmental issues intensifies, but the industry and standards are still evolving. Investors are left wondering how green the projects being funded truly are. According to BNN Bloomberg, approximately 90% of green bonds[2] issued are externally reviewed to ensure proceeds are used to finance or re-finance green projects. Investors should seek out green bonds that follow an established framework with recognized third-party verification.

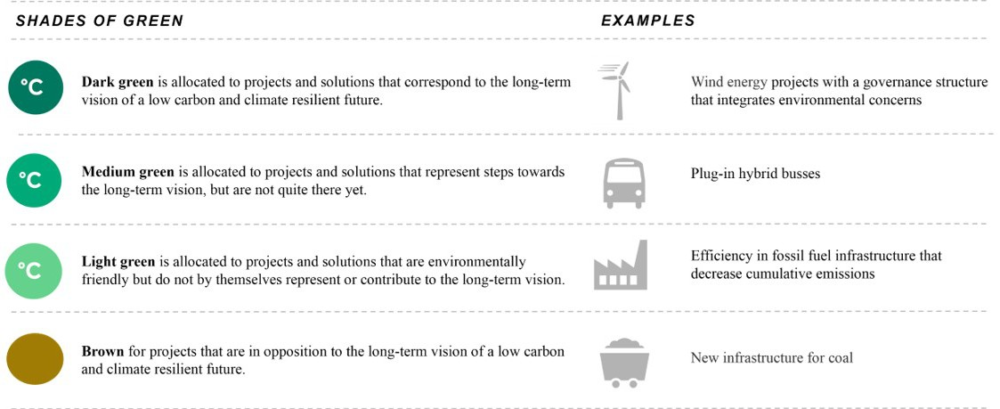

The most used frameworks are the Green Bond Principles, endorsed by the International Capital Market Association (ICMA) and the Climate Bonds Initiative certification. The largest third-party verifier against these standards, the Centre for International Climate Research (CICERO), builds on the guidelines to give investors an indication of how ‘green’ the projects are based on the projects funded. CICERO uses three shades of green: 1) dark green is for projects that correspond to a long-term low carbon and climate resilient future, such as clean, renewable energy; 2) medium green is for projects that represent steps towards a long-term vision, but are not there yet, such as plug-in hybrid buses; and 3) light green is for environmentally projects that do not alone contribute to the long-term vision, such as efficient fossil-fuel infrastructure. Such standards help investors select investments based on the level of environmental impact they would like to make in their portfolios.

Figure 1. CICERO Shades of Green

Green bonds are an innovative and important financial instrument to help achieve global and national emission targets. The green bond market has been growing rapidly over the past several years. In 2019, CDN$9.6 billion in green bonds were issued in Canada and US$255 billion were issued globally.[3] While this still represents a small portion of new bond issuances, this emerging sector is becoming more mainstream and on the radar for climate-conscious investors. For investors wanting to take climate action, green bonds provide a stable, predictable, fixed-income investment with measurable impact benefits.

Sources:

[1] Green with Envy: Canada’s Green Bond Market is Growing into a Global Player. https://www.dbrsmorningstar.com/research/344968/green-with-envy-canadas-green-bond-market-is-growing-into-a-global-player

[2] BNN Bloomberg – Canada leads in green bond deals as 2019 issuance hits $9.6B, above past years.

https://www.bnnbloomberg.ca/video/canada-leads-in-green-bond-deals-as-2019-issuance-hits-9-6b-above-past-years~1854214

[3] BNN Bloomberg – Canada leads in green bond deals as 2019 issuance hits $9.6B, above past years.

https://www.bnnbloomberg.ca/video/canada-leads-in-green-bond-deals-as-2019-issuance-hits-9-6b-above-past-years~1854214