Benchmarking Social Impact: How Investments Can Improve Communities

February 22nd, 2022 | Anna Murray

Historically, the primary mechanism for impact investment was the provision of finance through private equity investment or debt issuance. This could be explained, at least in part, by the clear link to the additionality of the financing; alignment with the longer-term nature of impact goals; and simpler impact measurement for project-specific financing.

In more recent years, the narrative around impact investing has evolved, leading to a greater appreciation of public equities as an asset class within impact investment. We see two key reasons for this:

– Addressing global challenges requires leveraging public equities, as they provide access to the vast capital needed to drive meaningful change. The persistent shortfall in achieving frameworks like the UN’s Sustainable Development Goals (SDGs) exemplifies this urgency.

– There have been improvements in the ability to measure the impacts—both positive and negative—of public equity investments. Given the value placed on impact measurement by investors, this development has increased the feasibility of public equities as an impactful asset class.

While impact investment in public equities is still in its infancy, we believe these factors will be foundational in the continued growth of the impact investment market in the future.

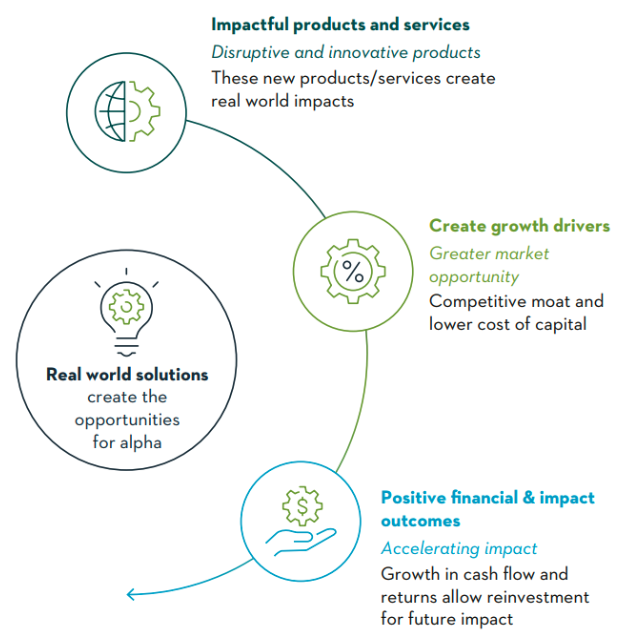

Impact-related assets under management globally are now USD 1.6 trillion, slightly more than one per cent of global AUM. As transparency has improved, public equity and public debt markets have experienced the fastest growth within the impact investing landscape. This rapid growth has not solely been due to a rise in altruistic investment; we, alongside other impact investors, believe that impact and financial performance can be positively interrelated.

Companies that create impactful and innovative products that address unmet societal needs can access attractive growth opportunities afforded by public markets. Quality companies should attract additional capital, , with profit generation allowing for reinvestment to generate further impact and compound returns for shareholders.

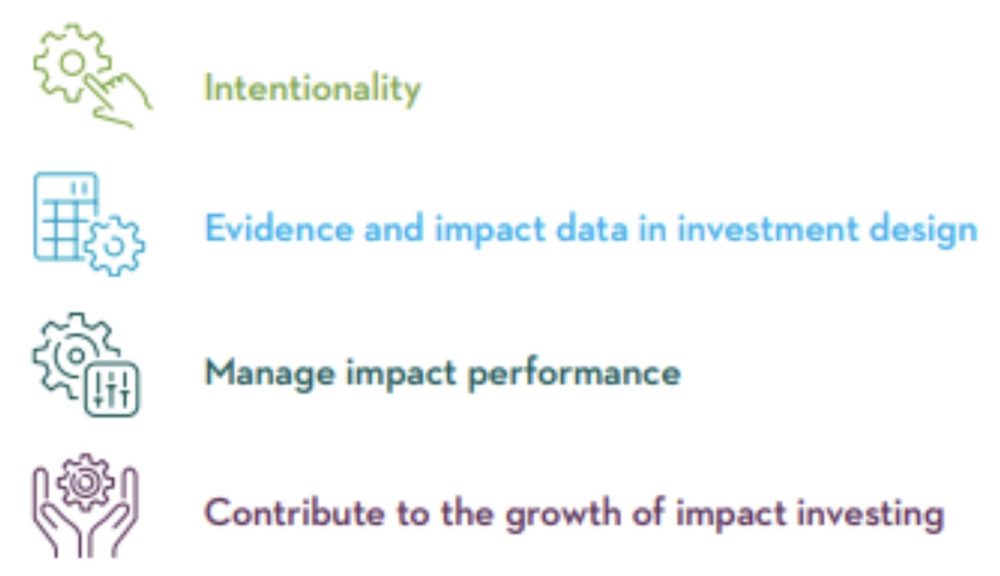

To truly balance the dual objective of positive impact and financial returns, there should be processes in place to establish a credible and authentic impact offering. The Global Impact Investing Network (GIIN) sets out four key characteristics of impact investing that we believe should frame any strategy, process or behaviour.

– Intentionality: We know that when investing, numerous biases and behaviours may lead to impact being de-emphasised in favour of chasing performance or reducing tracking error. To guard against this, there should be a clear mandate to invest in companies providing products or services that contribute towards an environmental or social objective, along with a theory of change for each investment. Impact should be a pre-condition for inclusion.

– Evidence and impact data in investment design: While we view intentionality as a precondition, this should be accompanied by analysis that sets out the impact the company is having in the real world. We believe that without a systematic approach to impact, one cannot provide evidence that holdings are relevant to the impact strategy and that they contribute to the impact objective.

– Manage impact performance: Once the presence of impact has been confirmed, its magnitude should be measured, encouraging accountability both for fund managers and the companies themselves creating tangible results to monitor and track. This can also be used to inform an engagement agenda for managers to accelerate the impact, a key additionality mechanism for public equity managers that could involve setting portfolio level or company level KPIs for reporting purposes.

– Contribute to the growth of impact investing: We advocate for an impact market with enough scale to deliver against the expectations of end investors. This could involve driving forward the impact investment market through innovation and best-practice sharing, acting as a long-term partner to investee companies and clients, and being transparent in approach, successes, and shortcomings.

These elements should not be totally new to investors. We regularly conduct detailed research and analysis. Looking through an impact lens is simply a new way of absorbing and processing company information, and we believe a methodical approach is important to avoid the above-mentioned biases.

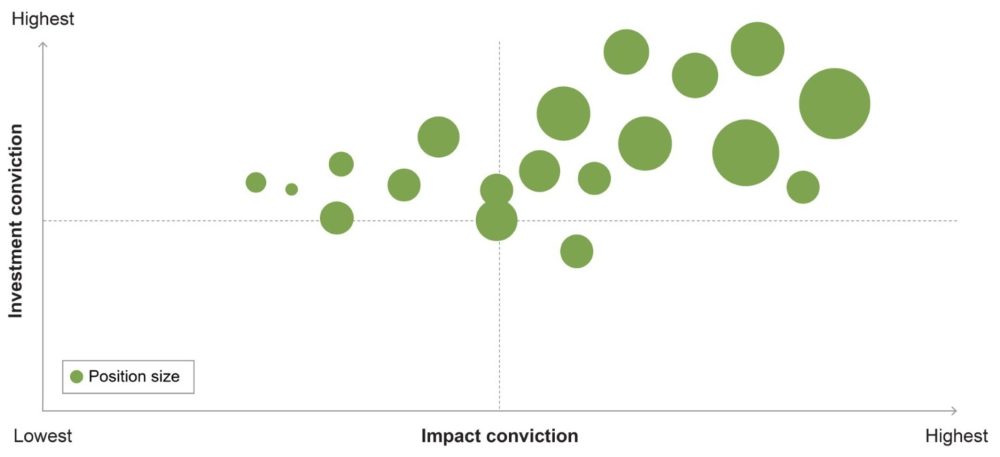

Below, we set out a possible way of integrating impact into portfolio construction decision-making by weighing investment and impact conviction equally when determining position sizes. This ensures that a focus on impact is maintained, while working to maximize returns within the opportunity set of impactful investments.

At the portfolio level, this could be represented by the diagram below:

However investors decide to integrate impact into their analysis and decision making, investing in public equities can provide impact at a scale that can only be achieved in public markets. We recognize that the companies in which we invest are likely to touch millions of lives each day, and we believe that more people are becoming explicitly aware of this, too.

As end investors seek to better understand the real-world impacts of their investments, rather than considering them as simply prices on a screen, we expect to see the impact investing market continue to thrive—and along with it, progress towards overcoming some of the greatest challenges we are facing as a society.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Franklin Templeton Canada 200

King Street West, Suite 1400,

Toronto, ON M5H 3T4

© 2025 Franklin Templeton. All rights reserved. Franklin Templeton Canada is a business name used by Franklin Templeton Investments Corp.

RIA Disclaimer

The views and opinions expressed in this article are solely those of the authors and do not necessarily reflect the view or position of the Responsible Investment Association (RIA). The RIA does not endorse, recommend, or guarantee any of the claims made by the authors. This article is intended as general information and not investment advice. We recommend consulting with a qualified advisor or investment professional prior to making any investment or investment-related decision.