Managed Phaseouts: an Investor Alternative to Divestment

August 19th, 2022 | John McHughan

Don’t Divest. Invest in Change

According to Bloomberg Intelligence, Global Environmental, Social, and Governance (ESG) assets are predicted to hit $40 trillion by 2030, despite macro challenges. Among the methodologies utilized, two common strategies that exist today are known as: ESG exclusion, the intentional exclusion of certain sectors or companies, and ESG integration, the integration of ESG factors into one’s fundamental analysis.

The exclusionary approach was one of the first iterations of ESG investing, resulting in the divestment from companies in sectors deemed “bad” or “brown,” excluding them from investment portfolios. Sectors commonly subjected to exclusion include weaponry, tobacco, coal, nuclear energy, and oil and gas.

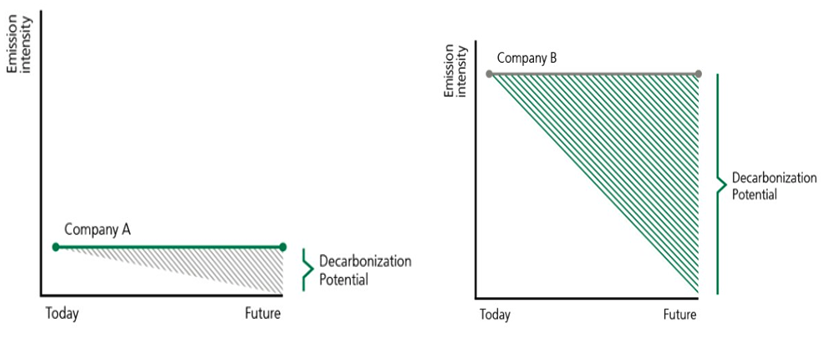

While the exclusionary approach can avoid exposure to these “bad” or “brown” sectors, studies have shown the long-term ineffectiveness in this approach. In a recent paper, Kelly Shue of Yale’s School Of Management and Samuel Hartzmark of the Carroll School of Management at Boston College, concluded “investing that directs capital away from brown firms and toward green firms may be counterproductive in that it makes brown firms more brown without making green firms more green”. When a heavily polluting firm is starved of capital, they are most likely to revert to the cheapest (and often most polluting) methods of production to continue to generate cash. If that same “brown” company wanted to improve their practices, while facing divestment, the firm would not have the capital required to make the investments and changes needed while conducting business as usual. Shue and Hartzmark also observed that a heavily polluting “brown” firm that reduced its emissions by just 1% would have a much greater impact than a typical “green” firm that reduced its emissions by 100%. See Figure 1 which highlights the decarbonation opportunity of a high emission intensity company.

Figure 1: Low emission intensity company (Company A) vs. a high emission intensity company (Company B)

Unlike an exclusionary approach, ESG integration does not limit the investable universe. Rather, it incorporates the consideration of ESG risks and opportunities into fundamental analysis.

A 2022 study by Capital Group found that 60% of investors cited ESG integration as the ESG approach most used. At Waratah Capital Advisors, we look for opportunities in “ESG improvers” that show positive ESG momentum through our ESG integration strategy that we have run since 2018. Consider a company with a historical reputation for poor ESG practices that is also behind its peers in implementing ESG considerations. The company would be deemed an ESG improver if it began demonstrating tangible ESG improvements. By providing capital to firms considered ESG improvers, we can help to “make the bad better” and be more impactful long term.

An example of a potential ESG improver is Canadian Natural Resources (“CNQ”). CNQ is one of the largest independent crude oil and natural gas producers in the world. Despite oil and gas companies often being in the spotlight for their negative environmental impact, they possess the ability to drive meaningful, positive advancements toward the world’s Net Zero target which is crucial in meeting the Paris Agreement. The International Energy Agency (IEA) has deemed carbon capture, utilization, and sequestration as an essential technology in their Net Zero by 2050 Roadmap. CNQ is currently the largest owner of carbon capture capacity in the Canadian crude oil and natural gas sector. Holistically, we believe their overall ESG practices are among the top of their peer group. We see CNQ in a position to lead peers as an ESG improver, not only in the net zero transition but also in industry ESG best practices.

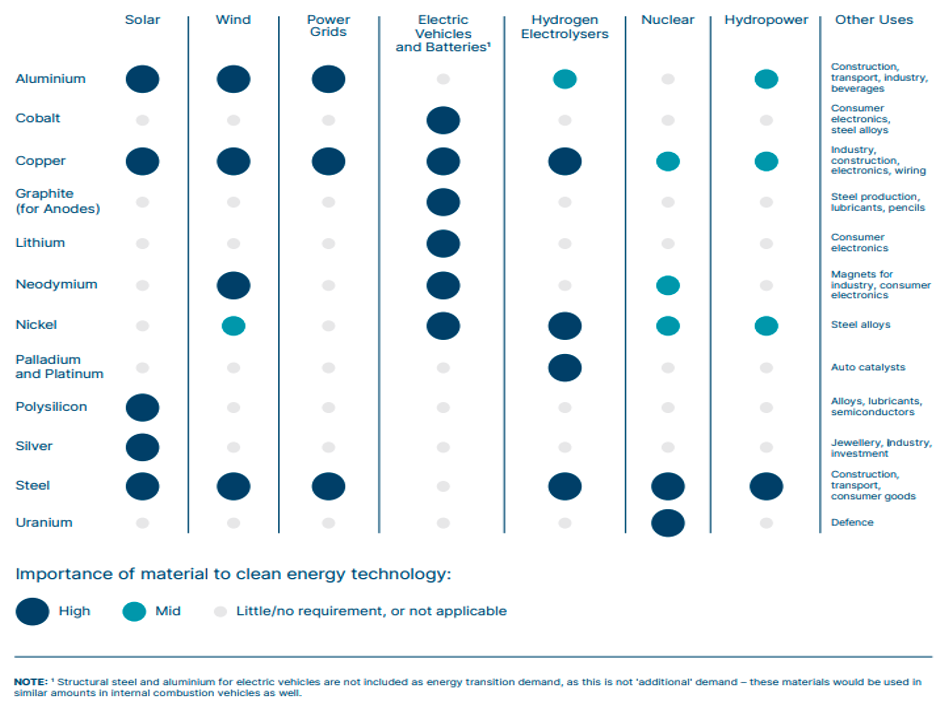

Companies within the mining sector have historically been viewed as negative ESG actors, due to the high environmental and social risks. The IEA deems several critical minerals, such as copper, lithium, nickel, and cobalt, as having an imperative role in the net zero transition. Mining companies, with exposure to energy transition minerals, will be essential to successfully build clean energy technologies. As shown in Figure 2, copper is of high importance to solar, wind, power grids, electric vehicles and batteries, and hydrogen electrolyzers as well as being of mild importance to nuclear and hydropower technologies. ESG improvers in this space show real signs of change, working on initiatives towards reducing emissions, improving operational efficiency, and demonstrating positive progress in their ESG performance data.

Figure 2: Materials used in clean energy technology

By solely divesting from a “brown” or “bad” ESG company, investors lose out on the opportunity to invest in change. ESG integration strategies allow investors to dig deeper into a company’s practices, compared to just looking at them from the surface through an exclusionary approach. Investors can put a spotlight on the “bad” ESG companies that are showing real signs of positive ESG momentum and in turn, have more opportunity and impact to make a change across all sectors.

RIA Disclaimer